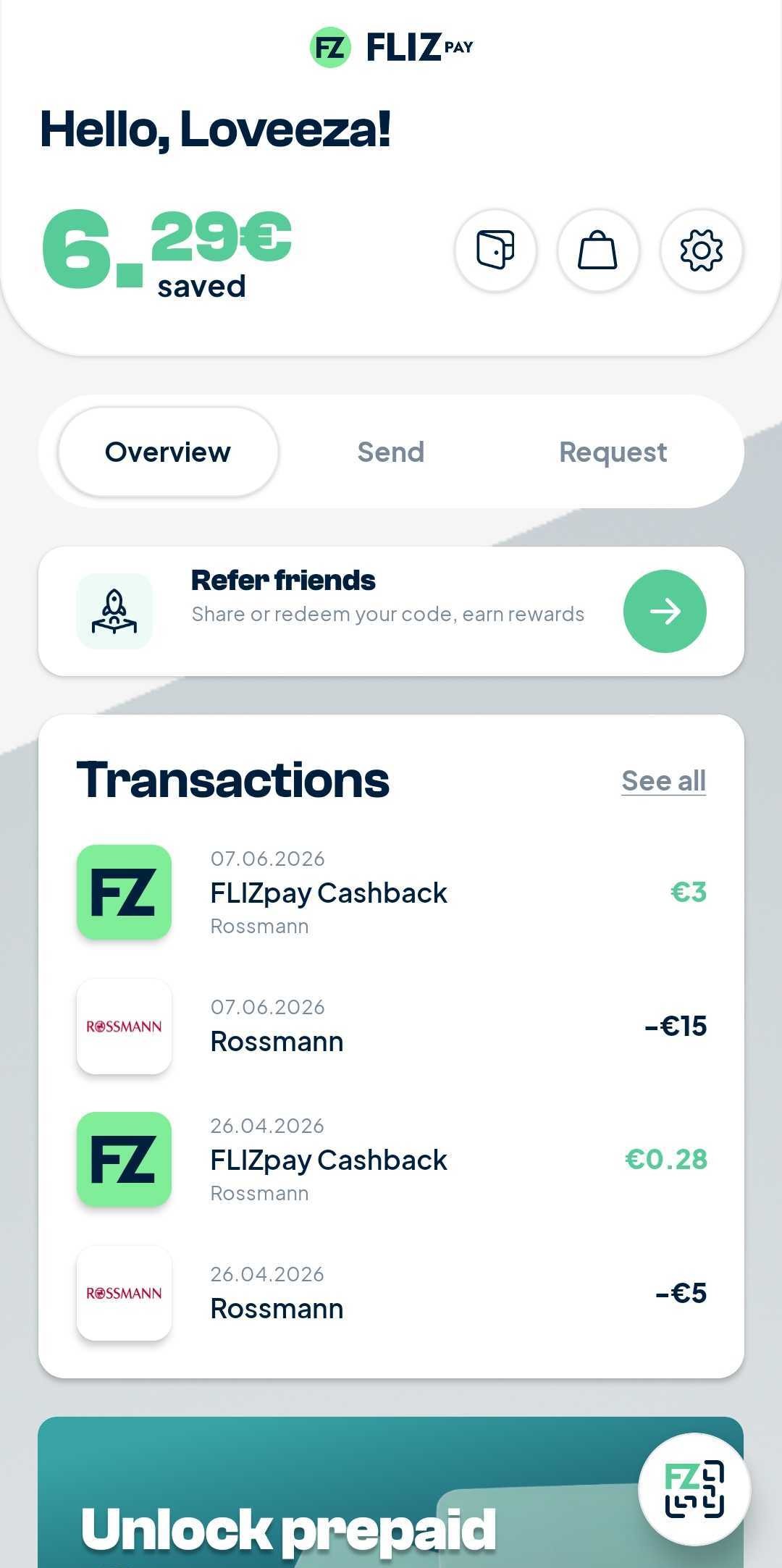

Flizpay is a Berlin-based payment startup that routes transactions via SEPA Instant Payments to cut the 1–7% fees card networks charge merchants. All data stays in the EU. Merchants pass those savings directly to customers.

A customer pays via Flizpay, the merchant absorbs less cost, and the user never notices. That's the model, and it works, but invisible benefits don't build daily habits. Payment apps with no rewards layer average 2–4 opens per month. Apps with active cashback programs see 3–5x that. Flizpay needed a reason for users to open the app before checkout, not at it.

The problem: building that in-house.

What European Fintechs Need to Know About Gift Card Integration

Most payment apps that want to offer gift card rewards hit the same wall. To do it yourself, you need to:

- Negotiate individual commercial agreements with each brand

- Build and maintain separate technical integrations per brand

- Handle inventory, settlement, and reconciliation across multiple suppliers

- Hire someone to manage it, pulling focus from the core product

Konrad's framing: "We cut fees and pass savings on, but gift cards extend that into very large discounts, without us handling every brand ourselves."

That's the gap finperks fills.

How finperks Works as a Prepaid API Layer for Fintechs

Every supplier contract, reconciliation process, and inventory management task that would have fallen on Flizpay's team was already handled on the finperks side. finperks is B2B API infrastructure for platforms that want access to prepaid products without building supplier management, catalog infrastructure, settlement flows, and market-by-market legal operations themselves.

What Flizpay's engineers actually built was the front-end experience: how users browse brands, select a gift card, apply their cashback, and track purchases inside the app. The back-end complexity never touched their roadmap.

For Flizpay, the integration replaced the entire brand-negotiation model with a catalog of diverse global brands available immediately: Adidas, Rossmann, Amazon, IKEA, Airbnb, and hundreds more across Germany and Europe.

The technical flow:

- Flizpay integrates the finperks REST API once

- finperks handles supplier contracts, reconciliation, and inventory

- Users browse, buy, and track gift cards natively inside Flizpay, while we handle the stock

What would have taken quarters of negotiations took days of engineering.

That process runs per brand. A catalog of 50 brands means running that sequence 50 times, often with different legal entities, different technical setups, and different commercial structures depending on the market. Germany, France, and Spain don't share the same brand entities or contract frameworks, so a pan-European catalog multiplies the complexity further.

With finperks, that entire sequence is already done.

Results: 50% Repeat Buyers and 25% New User Growth

The results that followed the integration weren't what Flizpay's team expected from a new feature rollout. Within the first weeks, 50% of users who bought a gift card returned to buy another one. That repeat rate pointed to something more durable than novelty: users had found a habit worth keeping.

At 8.5% of platform-subsidized buying on brands like Adidas, the economics were straightforward enough to act on. A user spending €100 gets €8.50 back, redeemable only on their next gift card purchase, which means every transaction feeds directly into the next one.

That redemption structure turns a one-time discount into a recurring revenue driver for Flizpay, and a recurring savings habit for the user.

The effect also reached beyond Flizpay's existing user base. 25% of new users during the period were attributed to the gift card offering, which meant the integration was generating acquisition, not just retention. Users were sharing the product because there was something specific to share: a discount they could put a number on. Tens of thousands of customers were now engaging with brands they hadn't previously accessed through Flizpay's payment core, deepening the platform's role in their everyday spending.

Opportunity: Promotional Features on Top of Closed-Loop Rewards

Flizpay has launched a refer-a-friend feature that ties directly into the gift card rewards system: when a user successfully refers someone, both parties receive boosted cashback on their next gift card purchase: a higher rate than the standard offering, applied automatically through the finperks catalog.

On top of other promotional features, such as earning a boosted cashback seasonally and Deal of the Week, where Flizpay boosts their current

With the payment infrastructure already proven and a rewards layer generating both retention and acquisition, Flizpay's next phase is one of depth rather than breadth, more brand categories, tighter loyalty mechanics, and a user base that keeps growing partly through itself.

About Flizpay

Flizpay is a Berlin-based fintech that routes business payments via SEPA Instant to cut card network fees. Their model redirects fee savings to consumers, with gift card cashback extending those savings further. In 2024, Flizpay raised €1M in pre-seed funding from Antler with fintech angels from Wise, SumUp, viafintech, etc.

This case study was produced by finperks in collaboration with Flizpay. Data reflects Flizpay's internal metrics post-integration.